- in Uncategorized by schooloftrade

Weekly Recap; Volume & Volatility reach EPIC Levels 3rd week of October

Volatility, and Trading opportunities the 3rd week of October! Oil plunges, stocks go bananas and the Bond Market, you had to SEE to believe! If you

missed the action, here’s your last chance to catch up!

levels this week!

S&P500 had given up than 4% on the week after a series of unfortunate

events hammered risk assets, drove liquidation and raised fear the dreaded

correction had arrived. However most of the gap was filled in the second half

of the week as the soothing possibility of more central bank easing emerged.

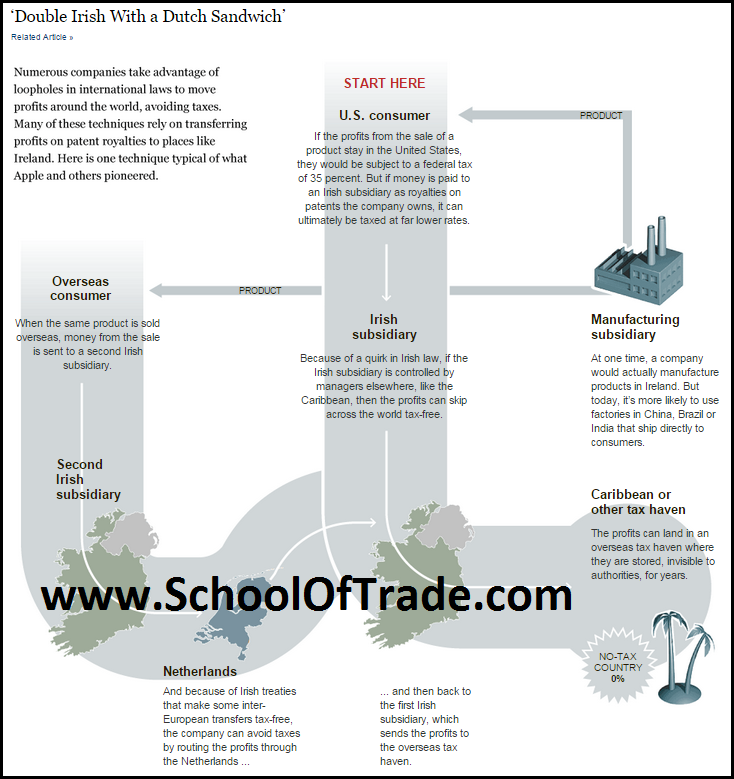

Ireland’s exotic tax avoidance laws, which inspired AbbVie to cancel its $54

billion merger with Shire, slammed many US hedge funds that were long Shire in

an arbitrage trade.

The same day, talk that the Greek anti-euro, anti-bailout

opposition had strengthened its influence drove a massive sell-off in European

peripheral debt, further hurting many US hedge funds that were long the

instruments. On top of that the Ebola scare reached a fever pitch with false

alarms across the US, though only one additional case was confirmed. The

combined effect was risk asset liquidation, driving the VIX index above 30 for

the first time in nearly two years.

action, Goldman Sachs’ CFO said investors were “shooting first and asking

questions later.” Then on Thursday, the ECB said it would adjust haircuts

on bonds used as collateral for loans to Greek banks and Fed Governor Bullard

said the FOMC should consider delaying the end of the QE taper this month to

help stem the slide in inflation expectations. Both announcements helped propel

a move higher, aided by some better US data late in the week and a round of

mostly solid earnings reports.

For the week, the DJIA dropped 1%, the S&P500 fell 1% and

the Nasdaq lost 0.4%.

correction territory on Wednesday, joined by the Japanese Nikkei Index on

Friday, while the S&P500 reached 9.5% off of September’s high before

rebounding. The market stampede was even more jarring in the bond market, as

the US 10-year dove 43 basis points between last Friday’s close and the height

of the fear on Wednesday before closing back at the key 2.20% level on Friday.

The data out on Wednesday suggested the global slowdown may be

finally catching up with the US economy. September US retail sales were negative (-0.3% v

-0.1%e; Control Group: -0.2% v +0.4%e), with the key control group, which is

used to help calculate GDP, way off expectations. That was the first negative

reading for the series since January, when severe winter storms depressed the

series temporarily. September PPI producer prices were softer than expected,

teeing up a soft CPI reading. The New York Fed’s Empire manufacturing index was

well under expectations, with the new orders component turning negative.

In Europe, markets tested Mario Draghi’s “whatever it

takes” position after developments in Greece provided an opportunity for

attack. Peripheral bonds sold off hard late on Tuesday and into Wednesday after

a poll in Greece showed the anti-bailout, anti-euro party Syriza with a 6.5%

lead over the governing New Democracy party, well ahead of the 1.4% lead seen

in the last round of polls. There is a presidential election in Greece in

February, which could be followed by early parliamentary elections. Greece’s

bailout is officially over in little more than a year, but PM Samaras would

like to end it early in order to get ahead of his Syriza opponents, who talk

often about getting Greece out of the eurozone. The rush to end 1% bailout

government financing and jump into public markets, at a rate more around 7% (or

the prospect of Grexit) drove the stampede out of Greek debt and a big drop in

the stock market, both of which shocked wider European equities and sent

peripheral debt spiking higher.

The Irish government confirmed that it will eliminate its notorious “double

Irish” tax structure, just a few weeks after the US Treasury said it would

put up roadblocks to tax inversion deals.

|

| Double Irish Tax Structure |

was the $54 billion AbbVie/Shire merger (Shire is headquartered in Ireland).

The implosion of the deal was cited as one of the factors deepening the

sell-off on Wednesday. Many hedge funds had long Shire/short AbbVie arb trades

riding on the merger and Shire shares lost over 20% as the deal unravelled,

pummeling the funds and forcing liquidation. Recall that back in July, AbbVie’s

CEO said the tax benefits were an advantage in the Shire acquisition but were

not the central rationale behind the deal. AbbVie will have to pay Shire $1.6

billion to break their engagement.

European governments are wrangling with 2015 budget planning and

the process is exposing many of the very stresses that have prevented the

Eurozone from escaping the long reach of its crisis. Budgets proposed by France and Italy both abandon

pledges to bring deficit-to-GDP ratios into compliance with the 3% treaty

limit. Last Friday S&P cut France’s sovereign outlook, and on Wednesday

Fitch put France’s AA+ sovereign rating on negative watch. German Chancellor

Merkel said there could be no exceptions to the EU deficit rules even as French

President Hollande demanded flexibility, setting up another axis of tension in

the EU.

The German government cut its GDP growth forecasts for 2014

(from 1.8% to 1.2%) and 2015 (from 2.0% to 1.3%), bowing to the reality of the

European economic slowdown. Berlin

insisted it would not change course on policy or austerity despite the worsening

outlook. Merkel said that the government would still pursue its balanced budget

goals.

The two cases of person-to-person Ebola transmission in the US

appeared in Dallas, Texas. Two nurses

who helped care for Thomas Duncan, the Liberian man who died last week, tested

positive for the disease. There was widespread consternation on reports that

the second nurse was cleared to travel to Ohio and back by air while also

beginning to feel certain symptoms, including fever, associated with the

disease. There was a cascade of Ebola scares in Ohio, San Diego, aboard a

Caribbean cruise ship and other locations from people who had unknowingly

travelled with the second nurse, although as of now there are still only two Ebola cases in

the US, the nurses.

The growing rift in OPEC pummeled oil prices this week, and

front-month WTI crude sank below $80 for the first time since June 2012.

Persian Gulf states were said to be targeting crude prices around $70 with the

aim of making US shale production uneconomical, and were

said to be opposing any OPEC production cuts at the November meeting due to

fears they could permanently lose market share. Non-Persian Gulf OPEC nations

plus Iran pushed for the organization to adopt a production ceiling of 30M bpd.

Venezuela called for an emergency OPEC meeting, but its demand largely fell on

deaf ears. The IEA Monthly Report trimmed global

oil demand growth forecasts for 2014 to their lowest level in five years and

also trimmed its 2015 demand forecast. The IEA said any more crude oil price

declines would require lower demand or supply cuts.

Wall Street banks had largely good news in their quarterly reports. Goldman

Sachs reported excellent third-quarter results and raised its dividend nearly

10%. Revenue was up 25% y/y and net income rose a whopping 60% y/y. Morgan

Stanley had similarly strong results. JPMorgan’s profits were slightly lower

than expected, but compared favorably with the loss seen a year ago. Bank of

America either reported income of $168 million or a small loss in its third

quarter, depending on how the bank’s massive $5.8B DoJ fine for mortgage issues

is counted. Shares of Citibank soared after the bank said it would exit

stagnant business in 11 countries and modestly topped expectations in its third

quarter.

Shares of railroad CSX gained after reports asserted that the company had

rebuffed a merger proposal from Canadian Pacific last week. If a deal were

reached, the companies would have a combined market value of $62 billion. Big

regulatory obstacles stand in the way of a merger – the US Surface

Transportation Board has a history of intervening in mergers over fears that

the industry would end up with just two North American transcontinental

railroad systems.

Overall volatility also whipped around currency trading this week, although

there appears to be a slight strengthening trend in the euro as the single

currency rises off the record lows seen in the first week of October. EUR/USD

came into the week around 1.2610 and after the excitement on Wednesday appeared

to be consolidating around the 1.2800 level. Meanwhile, the yen also

strengthened, with USD/JPY declining from highs of 107.70 to lows around 105.5

on Thursday, before closing out the week around 106.65.

The Shanghai Composite fell 1.4%, the biggest weekly decline in four months, as

the mainland index turned increasingly less immune to the global market rout

amid a set of mixed economic figures. September Trade Balance hit a 5-month low

of $31B, even though the y/y increase in imports and exports marked 7- and

19-month highs respectively. New Yuan Loans were also more encouraging at

CNY857B – a 3-month high and well above the CNY746B consensus. Inflation

indicators were still decidedly subdued however, as 1.6% CPI marked a near

5-year low while PPI of -1.8% was down on the year for the 31st consecutive

month. Monetary authorities are taking notice with further incremental

liquidity injection measures. On Tuesday, the PBoC lowered the offering yield

on its 14-day repo by another 10bps to 3.4%. On Friday, the PBoC also announced

an additional CNY200B injection directly into the banking system targeting 20

joint-stock Chinese banks. The balance of key China economic data for September

along with Q3 GDP will be released early next week, followed by the October HSBC

flash manufacturing PMI on tap for Thursday.

Click here to register for the

Free Trial!

Computer do the trading

trade Crude Oil

trade Euro

E-Mini Russell

Gold